Personal Finance

- What Net Worth Puts You in the Upper, Middle & Lower Class?

I found the graph at 10:55 to be especially interesting because it shows how someone with around the median income ($65k) can make it to the lower upper class by retirement through some discipline (10% saved per year).

As a quick TL;DW, here are the median incomes, net worth, and percent of population for each class:

- lower - $34k income, $3.4k net worth (many are negative) - 25%

- middle

- lower - $44k income, $71k net worth - 20%

- middle - $81k income, $159k net worth - 20%

- upper - $117k income, $307k net worth - 20%

- upper

- lower - $189k income, $747k net worth - 10%

- upper - $378k income, $2.5M net worth - 5%

Some questions to spark discussion:

- Do you agree with his breakdown of the economic classes? Why or why not?

- What strategies do you think someone in each category should take to improve their situation?

- If you don't mind sharing, what class do you think you're in, and does the breakdown match your experience?

- House refinanced 3x

My grandmother bought the home we lived in the 90s for 90k at a 8% interest rate. I found out she refinanced the house several times from what seems like predatory practices and malicious advice and now owes 250k at 6%. Basically the house I thought was paid off now has 30 mortgage and she is 90. Her grandkids are in the will to inherent the house but do we inherent this mortgage?

- TDF for house down payment

cross-posted from: https://lemmy.world/post/20168637

> Is a TDF a good choice for growing my money, in this case? I plan to use it for a house down payment and withdraw it in 5-7 years. I've been thinking of putting it in a 2030 or 2035 TDF. Should I go this route or just VTSAX and chill?

- Debtor Organizing Can Transform Our Individual Financial Struggles Into a Source of Collective Strengthinthesetimes.com Debtor Organizing Can Transform Our Individual Financial Struggles Into a Source of Collective Strength

Alone, our debt is a liability. Together, it’s our leverage.

- How to choose mutual funds to invest in

I've been on an HSA+HDHP for a couple of years now and only realized recently the interest earned from investing HSA money is also tax free, so I want to start investing a part of my savings and see how it goes. I have 2 options, Betterment or Mutual Funds. I figured I'd try the latter to avoid fees, but I'm not sure which funds to choose. My HSA currently provides 30 fund options.

I see people mentioning Vanguard a lot so I spread out my initial investment into 25% chunks across 4 different Vanguard funds. How did I choose them? Well I literally just looked at the performance graphs and selected the ones that historically went up steadily without major dips. As a total noob, how can I improve my choices? Is there a simple way to decide without having to dive deep into the stock market?

- Totally clueless with investing, $100k sitting in the bank earning 0.05%. How do I get started? Please advise.

I have been putting part of my paycheck into a high yield savings account, but haven't bothered with investing it in a responsible manner partially due a fear of losing the money due to bad investments. I'm finally realizing how much potential money I've lost by letting my money stagnate. Please advise me on how to responsibly invest my money, thanks!

- What do working Americans fear more than death? Retirement.www.usatoday.com What do working Americans fear more than death? Retirement.

These are the reasons some Americans are more scared of retirement than of getting divorced or fired.

- What has your experience been with a credit union?

I like the idea of a less profit-driven business that is maybe more community-focused but I wonder if they have the same capability as a bank? Have you been able to do your banking needs at a credit union? Was the customer service decent?

- Loan company hasn't reported to credit bureaus in 9 months

tl;dr - They haven't reported updated information since last year. How do I get them to do so, or how can I otherwise correct the information on my credit report?

Longer version:

Got a personal loan a few years ago through Lending Point. Earlier this year, I noticed that the last time they reported any updated information to the credit bureaus was December of last year. I paid the thing off back this past May, and had hoped that would trigger them to update it within a month or two, But they didn't, and as far as anyone(such as a new lender) is concerned, I still have an open personal loan that I owe a bunch of money on. Do I have to call these people and complain? Should I dispute the inaccurate information on my credit report? I spent quite a few years banging away at that stupid fucking thing, eliminating every negative account/collections/etc. Don't want to dispute that information just to find out that it's going to somehow backfire on me. As far as it stands now, I have no negative anything whatsoever on my report, and every single account on there is in good standing with a 100% perfect payment history.

Problem is, full-time job pays so little that for the last few years(basically since the pandemic started) I've been stuck more and more using credit cards and Affirm/After pay loans for "luxuries" such as... food, and having electricity, and clean clothes. You know, non-essentials. Using up more than half my (tiny) monthly income just to pay the minimums on the cards and the monthly Affirm payments at this point. Could use a new personal loan to consolidate all of that down to a single payment, but the fact that my cards are all maxed out is keeping my score down, making it difficult. And having it look like I already have an active personal loan when I don't, sure as shit isn't helping my case when trying to get a new one. Being able to consolidate would set me back into a position to where I have enough cash throughout the month to not have to rely on the cards to pay for basic shit in the first place.

- Survey: Almost 50% of Americans Consider Themselves ‘Broke’www.marketwatch.com Survey: Almost 50% of Americans Consider Themselves ‘Broke’

MarketWatch Guides surveyed different generations of Americans about their financial situation – and nearly half consider themselves broke.

- Fidelity 401k options

My employer recently switched to Fidelity and for now I've chosen the

LIFEPATH IDX 2050 Aoption. It looks like this one provides quarterly dividends, but the yield is 0.0%(?)I'm looking for some fairly risk adverse options or blends that provide dividends that will be reinvested. Anyone have any recommendations?

- Dow closes nearly 500 points lower Thursday as investors’ recession fears awakenwww.cnbc.com Dow closes nearly 500 points lower Thursday as investors’ recession fears awaken: Live updates

Stocks dropped Thursday as investors weighed the latest corporate earnings reports and economic data.

- Car Repossessions Surge 23% as Americans Fall Behind on Paymentswww.bloomberg.com Car Repossessions Surge 23% as Americans Fall Behind on Payments

High interest rates and tight budgets are making monthly bills unaffordable for a growing number of vehicle owners.

Paywall removed https://archive.is/NFELy

- Banks are bracing for consumers to stop paying off their credit cards, delinquency rates hit 12-year highqz.com Banks are bracing for consumers to stop paying off their credit cards

Provisions for credit losses rose at JPMorgan, Citi, Wells Fargo, and Bank of America last quarter

- 39% of Americans worry they can’t pay the billswww.cnn.com 39% of Americans worry they can’t pay the bills | CNN Business

Many Americans regularly worry they won’t be able to make ends meet.

cross-posted from: https://lemmy.world/post/17889213

> >Nearly four in ten (39%) of US adults say they worry most or all of the time that their family’s income won’t be enough to meet expenses, according to a new CNN poll. That’s up from 28% who expressed those concerns in December 2021, and it’s similar to the numbers seen during the Great Recession (37%). > > >To cope, significant shares of Americans said they are adding side jobs, cutting down on driving and putting more expenses on credit cards.

- CFPB cracks down on popular paycheck advance programs. Here's what that means for workerswww.cnbc.com CFPB cracks down on popular paycheck advance programs. Here's what that means for workers

The watchdog proposed a rule that would label earned wage access programs as loans. Fees would need to be expressed in APR terms, like a credit card.

- How do I make enough money to live?

Yes, I do have a full-time job, and I even enjoy it, but it doesn't pay enough to survive in this hellscape of a world we live in. I lack the college degree required to get almost any decent-paying job (plus my last job hunt took MONTHS to get a lead), I don't have the skills or originality to become an online content creator, nor the artistry or patience to create and sell trinkets on Etsy (plus, that would require an initial investment which I simply do not have). Should I set up a GoFundMe? OnlyFans? I wouldn't really be offering anything except a charity basket/collection plate so that feels dishonest at best. Idk, I'm quite literally having a breakdown because I'm probably going to lose my car soon, and then my job, and then my apartment, and then my life. Any help at all would be appreciated. Thank you

- Nearly half of Gen Zers get help from the bank of mom and dad, report findswww.cnbc.com Nearly half of Gen Zers get help from the bank of mom and dad, report finds

Today, 46% of Gen Zers rely on financial assistance from their family to get by, according to a new report from Bank of America.

- More People Make 'No-Buy Year' Pledges as Overspending or Climate Worries Catch Up With Themwww.kqed.org More People Make 'No-Buy Year' Pledges as Overspending or Climate Worries Catch Up With Them | KQED

A 35-year-old Brooklyn resident gave up buying new clothes. A 22-year-old in San Diego swore off retail therapy at Target. A 26-year-old in England banned carbonated drinks from her shopping list. These three women, who don’t know each other, all started the year resolving to spend money only on nec...

- JPMorgan Chase warns 86 million customers they might have to start paying for their bank accountsfinance.yahoo.com JPMorgan warns 86 million customers they might have to start paying for their bank accounts

Bank prepares to pass costs on to customers.

>The potential charges, says Marianne Lake, CEO of consumer and community banking at JPMorgan, are a result of new regulatory rules that cap overdraft and late fees. Lake says Chase will be passing along those increased expenses to customers, which would put an end to now-free services such as checking accounts and wealth management tools. And she says she expects other banks will follow suit.

- California to make financial literacy classes a requirement to graduate high school [USA]abc7.com California to make financial literacy classes a requirement to graduate high school

Governor Gavin Newsom announced on Thursday an agreement that requires all California high school students to take a semester-long personal finance education course starting by the 2027-28 school year.

- Best way to buy a house for another person? [USA]

I'm in an extremely fortunate position where my Mom, upon learning about current mortgage rates and why I haven't bought a house yet, wants to essentially be my bank to buy a house. As in, she wants to fund the house, put it in my name, and I pay her a reasonable down payment and pay a "mortgage" to her at 2-3%. So what would be the best way to do this?She buys the house then transfers the deed? Should she just transfer the cash and I purchase it?

Side note: I know people are usually against doing big purchases with family, but I don't really see a downside since the house will be in my name, and with that 2-3% rate, the payments will be similar to my rent even considering maintenance and property tax.

- USA: The financial meltdown is beginning.www.nbcnews.com The collapse of a fintech firm with 10 million users has left many Americans without access to their money

A court dispute has ensnared potentially millions of Americans, leaving them without access to their money for nearly two weeks.

They are keeping this quiet, but this affects 2.9% of US bank customers.

- We shouldn't have to work 40 hours a week to afford a basic life. We do because our currency is constantly losing value. This is by design.

There's a lot of talk about inflation and its causes. Is it corporate greed? Supply chain issues? One clear base cause of inflation less talked about is having an inflationary currency supply. Any other inflation caused by supply chain issues, corporate greed, lack of market competition, etc is just added on top of that. Fiat inflationary currency is a rather new invention in terms of the human timeline. In the US, Nixon is the start of it. Central banks aim for 2-3% inflation in "good years". The money supply expands, the portion of that supply a single dollar represents, and therefore its value, decreases. This isn't a conspiracy, it's government policy, and both parties gleefully support it because it benefits their rich donors.

Think of it: in the last 50 years, everything has gotten cheaper to produce thanks to increasing mechanization, outsourcing to cheap labor/low regulation countries, and extremely efficient supply chains. Yet so many things "cost more" than they did 50 years ago. Even basics like bread. What used to be 5c in the US in the 50s now costs $5.00. How is that the case? Shouldn't it cost less? Where is that "extra efficiency" going if not to lower prices? The answer: bread is the same value it's always been, the money has gotten less valuable. This is how they keep working class people running on a treadmill, never able to achieve economic mobility.

Inflationary currency devalues the currency you worked hard to earn by increasing the supply. It hits the middle class the worst because they have more of their net wealth in cash, often in the form of emergency funds, savings, and putting together enough money for a down payment on a home. Rich people have their money in assets which aren't harmed by currency inflation. Actually, even worse, it inflates the value of those assets! If the dollar loses value (all other things being equal), it takes more dollar to buy a share in Amazon, just like it takes more dollars to buy a loaf of bread. Poor people live hand to mouth, so their net wealth is not impacted much, but inflationary currency prevents them from saving and "moving up". If you want to identify the causes of increasing wealth disparity, the inability of people to save money and theft of value from the middle class via money supply expansion is a major one.

- Please explain leverage to me

can someone explain leverage to me as practised by those RE

bullshittersfinfluencers. I feel their whole spiel is just bullshit but I don't know enough to be sure about it.according to them, you "buy" a home - you put X% down and pay your first monthly (and then post on r/firsttimehomebuyer). then you go to (another?) bank and say "look I got this house I wanna use as collateral" and they go "wow you own a house! sure, have this bag of money"... repeat until you "own" like a city block.

like, how does that not crash and burn at the first step, just a cursory glance at the asset's status? how are they not "lol you ain't got no house dumbass come back in 20 years when you actually own it"?

- Inflation is higher than they would like you to believe.

The US government is telling everybody that inflation is 3.4% per year. That is not correct. Try 14.2% and that's about right. Source : gold/usd 1 year simple moving average.

- Wealth inequality starts at birth. Lawmakers debate whether child savings accounts can helpwww.cnbc.com Wealth inequality starts at birth. Lawmakers debate whether child savings accounts can help

The 401Kids Savings Act would create savings accounts for newborns. While state child savings accounts have shown promise, inflation and taxes prompt concerns.

- YNAB vs Quicken Simplifi

I wanted to start using a budgeting program to better organize my spending/ goals, and basically narrowed it down to 3 --YNAB, Actual and Quicken Simplifi.

I setup a self-hosted instance of Actual and was able to import my spending from my account by exporting from my bank and importing into the app, however this seemed like it might get tedious over time, so I decided to try YNAB.

So far this has been pretty straight forward. I’m still waiting for things to sync up with my linked accounts, but I like it so far. I would try Simplifi but there’s no trial period there; though the graphs and UI make it seem appealing.

Anyone here have any experience with Simplifi/ YNAB, and why might you chose one over the other?

- The best european online card that doesn't block your account

I'm looking for the top European bank that doesn't block your funds without reason. For instance, many individuals have reported online that Revolut has blocked their accounts suddenly and sometimes for various months.

- Recommendation for software/ apps

Hello,

So I recently revisited (and recreated) my savings spreadsheets so that I can track my

needs,wantsandsavings. To try to keep track of myfixed costsand also try to follow the50/30/20rule (not sure if this is a good strategy or not).I have everything mostly sorted, but as new things come up, say a new subscription or a cancelled one, changes in rent, etc. It will be a bit of a hassle to keep this up to date.

Are there any software/ apps that you guys use that you like that make this kind of thing easier to see where your money is going?

- Was the 401(k) a Mistake? How an obscure, 45-year old tax change transformed retirement and left so many Americans out in the cold.www.nytimes.com Was the 401(k) a Mistake?

How an obscure, 45-year-old tax change transformed retirement and left so many Americans out in the cold.

- Selecting a CFP - not just the basics

How would you go about selecting a Certified Financial Planner?

My wife and I are financially successful adults, but we need guidance with the next steps, including:

- Private equity co-investment

- College savings for children with special needs who may or may not attend university

- Retirement savings beyond the standard 401k and IRA options

- The tax ramifications of all of the above

My friends are generally not at this level of planning needs, so those who have worked with a CFP have had only much more basic questions. We have known plenty of financial advisers over the years who just give bad advice or canned advice. I expect our needs will become more complex over the next decade.

How do we find a quality CFP who can help with the above? What is a reasonable price to pay for this help?

Thank you for taking the time to share your thoughts!

- Americans are falling behind on their paymentswww.cnn.com Analysis: Americans are falling behind on their payments | CNN Business

America’s relentless spending has kept the economy motoring. But it’s starting to worry some observers.

- Home prices have outpaced inflation by 2.4 times

cross-posted from: https://lemmygrad.ml/post/4307103

> Home prices have outpaced inflation by 2.4 times

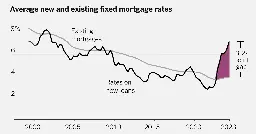

- A Huge Number of Homeowners Have Mortgage Rates Too Good to Give Upwww.nytimes.com A Huge Number of Homeowners Have Mortgage Rates Too Good to Give Up

On a scale not seen in decades, many Americans are stuck in homes they would rather leave.

- The craziness of the US stock Market

cross-posted from: https://lemmygrad.ml/post/4277310

> The craziness of the US stock Market